About two years ago, I had an extensive discussion with François Darchis, Senior Vice-President of Air Liquide, on how to build competitive advantage. He indicated that the company had pursued multiple strategies to develop a sustainable competitive advantage. Implemented strategies included:

- cost reduction

- operational excellence

- Geographic expansion in BRIC countries (Brazil, Russia, India, China)

François Darchis also told me that he was adding a new strategy to building competitive advantage: innovation. So I asked Luka Mucic, CFO and COO of SAP, where innovation fits in building a competitive advantage.

I/ Introducing Luka Mucic

A member of the Executive Board and Global Managing Board of SAP SE, Luka Mucic handles all corporate financial activities as well as administration of the company and has served in this function since July 2014. In addition, Luka is responsible as COO for the Process Office of the company.

He began his career at SAP in 1996 as a member of SAP’s Corporate Legal department, where he focused on corporate and commercial law. Luka holds a master´s degree in law from the University of Heidelberg, Germany, and a joint executive MBA from ESSEC, France, and Mannheim Business School, Germany.

II/ Innovation is a critical component of SAP’s strategy

Luka told me that before answering the question he needed to give some elements on the context. The role that innovation plays in a company’s strategy is very much a function of its industry.

- In traditional industries like automotive, the focus is very much on optimizing operations with existing assets and on expanding geographically. Leaders try to reduce cost while keeping the product output pretty much the same. Management focuses very much on cost reduction strategies. Innovation is driven by a small group.

- In technology-driven industries on the other hand, innovation plays a more important role. For example, at SAP, innovation is viewed as a key lever in creating a sustainable competitive advantage and maximizing earnings per share.

IT companies tend to be profitable. Therefore, Luka can mathematically model the added earnings per share that he would get if he pursued cost reduction strategies. Equally, one can mathematically model the incremental earnings per share one would get when implementing revenue-generating activities like innovation. It turns out that, in profitable industries, pursuing revenue-generating activities like innovation almost always end up creating higher earnings per share than cost reduction strategies.

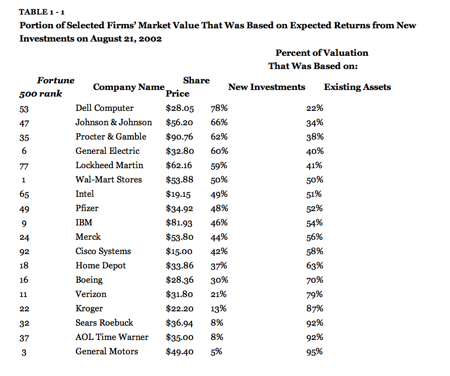

Innovation is a critical element of SAP’s competitive strategy portfolio because it produces more earnings per share than alternative strategies. This reminded me of a table in Clayton Christensen’s Innovator’s Solution. I shared it with Luka to get his perspective.

III/ Innovation is a share price booster

This table shows that the valuation of shares is based on existing assets and future assets.

- In traditional businesses like automobiles, the financial community tends to equate corporate shares with existing assets. For example, General Motors’ share is for 96% a function of its existing assets. The financial community doesn’t value future assets that the company may produce, probably because they have little confidence in the company’s ability to innovate. Thus, management focuses on reducing costs in existing assets more than pursuing innovation strategies. Luka pointed to me that the table provides an excellent illustration of the point he made earlier.

- Industries like IT industries and pharmaceutical industries that rely heavily on innovation enjoy higher valuations. In fact, their shares are only partly a function of existing assets. The financial community believes in these companies’ ability to innovate which leads them to value future assets heavily. SAP is comparable to Intel in the table. In other words the Earnings-Per-Share account for about 40 or 50% of existing assets and 50 to 60% of future assets. The financial community anticipates that SAP will be able to create new revenue in the next few years because of their culture of innovation. They are confident that SAP will be able to generate additional revenue with products that perhaps don’t exist today or at least that have not generated revenue today.

This seems to be a reasonable valuation according to Luka. Indeed, Luka indicated to me that only five years ago, a number of different products, critically important today, did not exist. For example, Hana did not exist. And yet this product has great potential. In the first half year of 2015, SAP HANA continued to be a major growth driver for the Company. The number of SAP HANA customers surpassed 7,200, almost doubling from just one year ago. “Cloud and software revenue grew by 23% and increased our operating profit by 14% surpassing € 2.4 billion in a first half year”, according to Luka.

IV/ To sum-up : Innovation is a share valuation booster

So this pretty much summarizes my discussion with Luka. Innovation is a critical component of SAP’s competitive strategies for multiple reasons:

- In technology-driven industries, innovation plays a critical role in share valuation as investors reward companies that have demonstrated an ability to generate new revenue.

- In more traditional industries investors tend to reward cost-cutting strategies rather than innovation as such.

- A company like SAP has an ability to create revenue-generating products in a very short time span. Products like Hana and many others didn’t exist only a few years ago and today they represent a considerable part of the revenue.

But, how to make innovation happen? This is the topic of a follow-up discussion…

[…] About two years ago, I had an extensive discussion with François Darchis, Senior Vice-President of Air Liquide, on how to build competitive advantage. He indicated that the company had pursued multiple strategies to develop a sustainable competitive advantage. […]

[…] the short-term, “innovation is a share valuation booster”, as Luka Mucic, CFO of SAP once told me during an interview for The Innovation and Strategy […]

[…] venturing in white spaces seems risky, shareholders reward forward-looking companies with higher Earnings Per Share (EPS), according to Luka Mucic, CFO of […]